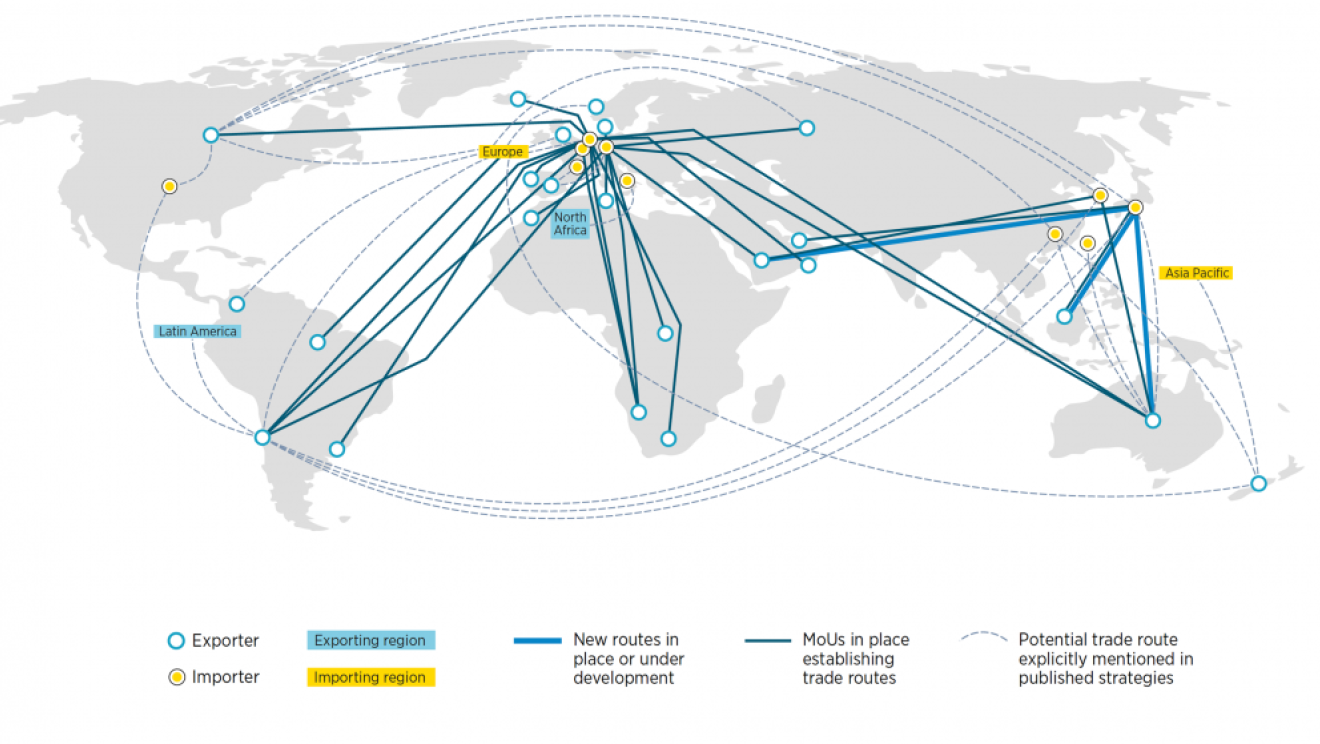

Countries in the “Global South” with a high low-cost hydrogen potential are developing export-oriented hydrogen sectors. This entails support for the development of appropriate infrastructure to produce and export hydrogen. For example, auctions have been held in Chile to support the deployment of the first 388 MW of GH2. Colombia’s GH2 strategy includes measures to support both hydrogen shipping capacity to meet expected international demand as well as firms’ export ambitions, while promoting the country’s role as a prospective logistics hub in the Caribbean.

If carefully planned, GH2 can induce a geopolitical shift in production, trade and energy security to the benefit of the Global South. As discussed in the anchor piece for this GH2 series, countries in the Global South are likely to benefit from new paths to industrialization which a shift to GH2 would create, thereby generating new jobs and additional welfare benefits. The relocation of manufacturing would be most suited for industrial commodities such as aluminium, ammonia, iron, jet fuel and methanol. Three elements can drive this phenomenon2, namely (i) the willingness of industrial agglomerates to relocate; (ii) the cost of transporting finished or semi-finished products compared to the transport of energy, and (iii) the cost of energy.

Setting up new production facilities in renewables-rich countries does not necessarily imply the closure of plants elsewhere. On the contrary, the energy transition offers scope for growth in many industries. More ammonia will be needed to fuel international shipping and more steel will be required, given the expected population growth and the energy sector’s new infrastructure requirements.

Transporting green goods will be cheaper than transporting GH2. Energy-intensive industries have the opportunity to establish new facilities in countries with low-cost renewable surpluses, exporting semi-finished products (e.g. reduced iron) or finished goods (e.g. cars); the cost of energy may be a key factor in their decision.

The potential of renewable energy and land availability in the Global South create a major competitive advantage for regions with surplus renewable resources to become sites of green industrialization. Even though the cost of renewables is falling across the globe, sizeable differences in terms of cost between countries and regions remain. Therefore, energy sector policies to reduce the political, regulatory and financial risks that renewable energy developers might face are instrumental for decarbonizing the local energy sector and attracting green industrialization.

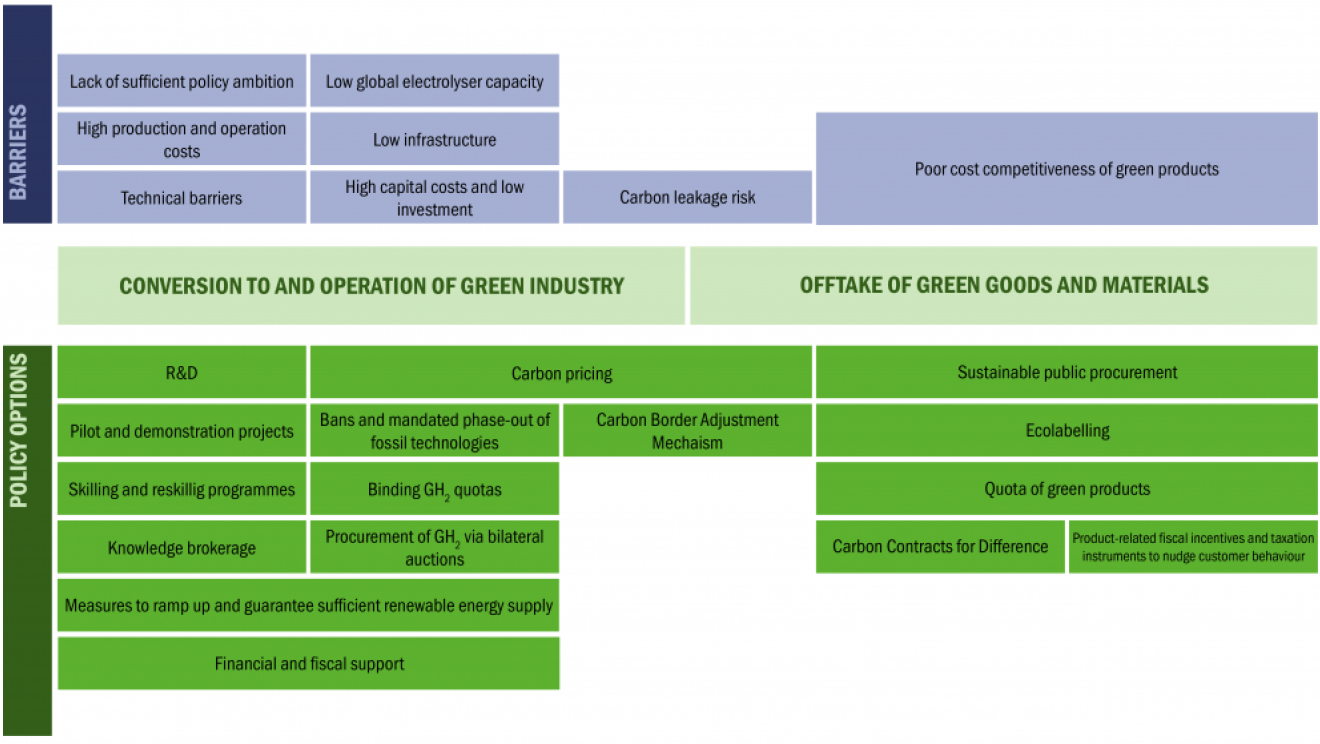

Industrial policies to support GH2 supply and demand are still in their infancy and are mostly drawn from policies that were once used to promote the uptake of renewable energy. Yet differences between the two cases exist and adjustments will have to be made as we learn by doing. Nevertheless, this should not prevent any country from establishing a GH2 sector and from sharing its experiences.

Green Hydrogen can induce a geopolitical shift in production, trade and energy security to the benefit of the Global South

- Emanuele Bianco is Programme Officer at the International Renewable Energy Agency (IRENA).

- Manuel Albaladejo is Country Representative for Argentina, Chile, Paraguay and Uruguay, at the United Nations Industrial Development Organization (UNIDO).

- Smeeta Fokeer is Industrial Development Officer at the Climate and Technology Partnership Division (CTP) of the United Nations Industrial Development Organization (UNIDO).

- Nele Wenck is Junior Specialist at the United Nations Industrial Development Organization (UNIDO) and PhD student at Imperial College London.

- Petra Schwager is Chief of the Energy Technologies and Industrial Applications Division at the United Nations Industrial Development Organization (UNIDO).

Disclaimer: The views expressed in this article are those of the authors based on their experience and on prior research and do not necessarily reflect the views of UNIDO (read more).